")

")

")

What Causes Subscription Chargebacks?

Subscription-based sales can be an excellent way to build long-lasting customer relationships and establish an ongoing revenue stream. Subscriptions build customer loyalty, and that’s according to the metric that matters most—sales. Customers are 75% more likely to make additional purchases from a merchant with whom they already have a subscription or similar preexisting relationship. Statistics like these have been fueling the subscription industry’s massive growth in recent years, and according to Juniper Research, subscriptions worldwide could grow by as much as 200% by 2026.

Unfortunately, increased transaction volume always brings a commensurate increase in things like fraud and chargebacks. Fraudsters deliberately target fast-growing markets, hoping to take advantage of merchants who are too busy dealing with incoming orders to look too closely for fraud indicators, and customers who are new to subscription billing models—or e-commerce in general—often file illegitimate chargebacks out of frustration or confusion.

Subscription payments tend to turn into chargebacks more often than the average one-time payment, and that can lead to problems for merchants. Each chargeback causes losses that include the revenue from the sale, the chargebacks fee, and any costs related to acquiring the customer and making the sale. In addition, an excessive chargeback rate can lead to harsh fines and even the termination of merchant accounts in extreme cases.

In order to avoid these consequences, merchants need to determine the root causes of their chargebacks and make changes to reduce future disputes. In collaboration with Juniper Research, Chargeback Gurus has authored a whitepaper that analyzes the root causes behind chargebacks and other payment challenges in the subscription market. Here are some of the key takeaways.

Chargebacks: The Facts

Each chargeback comes with a reason code that specifies the type of fraud or customer dispute it’s based on. If the dispute claims are invalid, the merchant can represent the charge, along with compelling evidence, to persuade the issuer to reverse the chargeback. When no resolution can be reached, the card network may be asked to arbitrate the dispute.

Identifying chargeback reason codes is key to analyzing the causes behind payment disputes and determining the proper response.

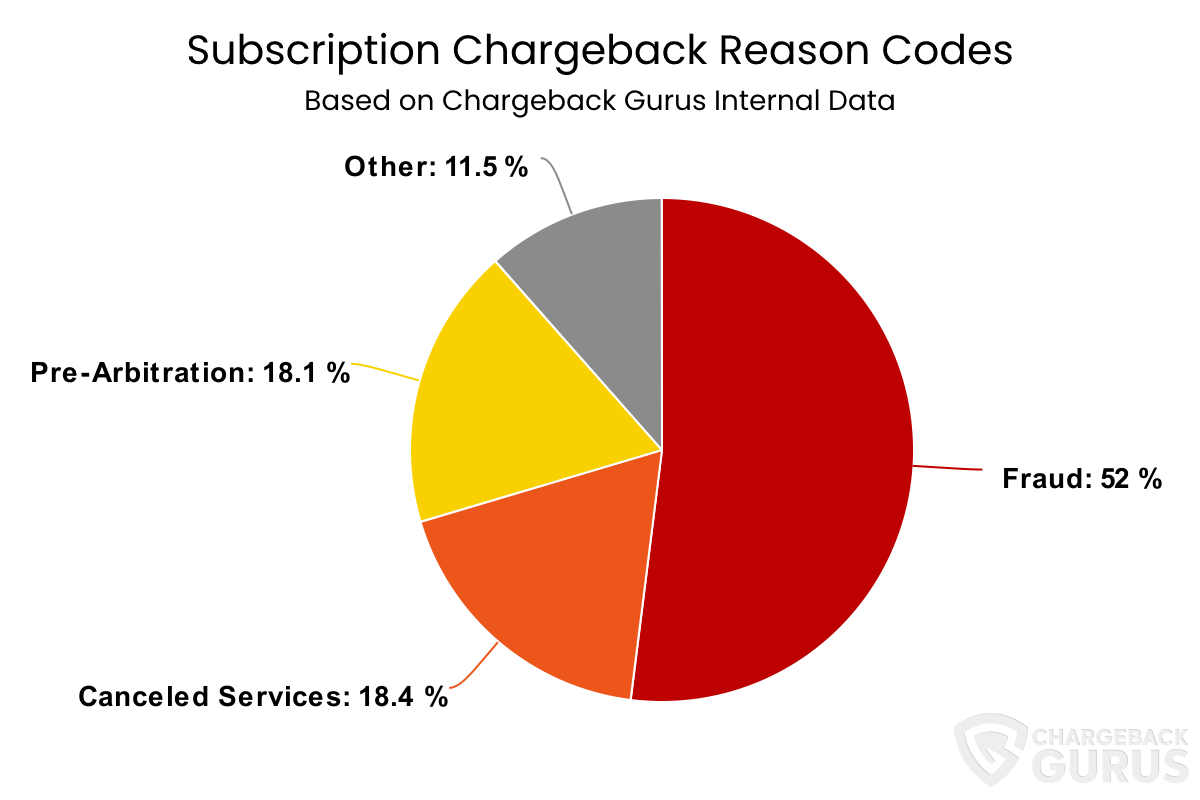

The Most Common Reason Codes for Subscription Chargebacks

In the subscription market overall, claims of fraud account for a majority of payment disputes. Canceled services is the next most common reason code, which should come as no surprise. The third most common reason code, pre-arbitration, is more interesting. It indicates that it’s relatively common for issuing banks to decide in a merchant’s favor, then reverse the decision and send the dispute back to the merchant. This often indicates that the merchant was unable to make an airtight case that the charge was legitimate.

The new rules established by Visa’s Compelling Evidence 3.0 update may serve to reduce this issue. If the merchant can satisfy the requirements of CE3.0, the case permanently decided in the merchant’s favor, eliminating the possibility of pre-arbitration.

Digging Deeper: Industry Analysis

While no two merchants will get exactly the same chargebacks for the same reasons, there are definite patterns depending on the market you serve. Chargeback Gurus analyzed chargeback reason codes across various subscription-based verticals to obtain deeper insights into the causes of subscription chargebacks by industry. Here’s what they found:

- Computer Software: Canceled Services was the most common chargeback reason code, outpacing even claims of fraud. Information Technology and Services had similarly high rates of this reason code. This may indicate that customers often find it difficult to cancel their subscriptions and end up disputing charges instead.

- Consumer Services: Fraud made up nearly two thirds of the chargebacks in this category, as was also the case in Financial Services and Retail. Merchants in these industries will want to make sure their fraud detection is robust and accurate.

- Digital Services & Entertainment: These industries had the highest rate of fraud chargebacks at 73% and 72%, respectively, indicating that this category is a prime target for credit card thieves. While they can cause customer friction, stricter anti-fraud protocols are the most effective solution here.

- Energy: A third of all Energy chargebacks ended up in pre-arbitration, which tells us that dispute outcomes in this category are not easily accepted by either party.

- Health, Wellness, and Fitness: Services Not Provided cracked the top three reasons for this category. That’s a clear indicator that dissatisfaction is high in this industry, with many customers feeling like they didn’t get what they paid for.

- Insurance: High rates of both pre-arbitration and Services Not Provided chargebacks prevailed here, which may point toward confusion over terms and difficulties with customer service. Marketing and Advertising and Real Estate Services were in similar situations, but with even higher Pre-Arbitration rates.

- Warranty and Repair Services: Canceled Services took the top spot here at 30%. This may be partly due to the fact that these services often bill on an annual basis, and they’re easy for customers to forget about.

Understanding and Preventing Subscription Chargebacks

The statistics above tell a number of stories about why and how chargebacks occur in the subscription economy. Most of the time, the story is fraud, and the only way to deal with fraud at scale is to block it with tougher security protocols and automated tools that can detect attacks in real time.

The rest of the chargebacks center on customer disputes, and many of them can be traced back to difficulties with automatic recurring billings. Customers forget about the services they’ve subscribed to, especially when charges are annual or otherwise infrequent.

They may file a dispute because they no longer recognize a charge, or because they find it easier than figuring out how to cancel their subscription directly.

Chargebacks like these are illegitimate. With the right evidence, such as proof that they agreed to your terms and conditions or failed to make use of an accessible cancelation feature, merchants can fight these chargebacks and recover their revenue—but it’s always cheaper and more effective to prevent them from happening in the first place.

Here are a few prevention tips for subscription merchants:

- Make sure your sign-up, billing, and cancelation policies comply with card network regulations.

- Make it fast, easy, and convenient for customers to cancel their subscriptions.

- Process requests immediately and notify the customer when you have done so.

- Always obtain a new payment authorization from returning customers—don’t just charge their card on file.

- A few days before billing, notify customers that their card will soon be charged.

- When subscription rates go up, notify customers in advance and obtain a new payment authorization.

- Your merchant descriptor, the information that appears on cardholders’ billing statements, should make it easy for customers to identify you immediately and look you up online.

The best way for merchants to deal with chargebacks is to follow a comprehensive chargeback management plan.

This can involve ongoing data analytics, a strategic approach to representment, and partnerships with vendors who have a deep understanding of both your own industry and the electronic payments ecosystem.

By taking the time to understand the origins of your chargebacks, you can implement effective prevention measures to keep your revenue safe and improve customer relations.

For more data on subscription chargebacks, as well as a look at decline rates and decline codes by industry, check out the full whitepaper here.

| Tagged with: | fraud |

| Posted in: | AF Education |